February 6, 2026

“All That Glitters Is Not Gold?“

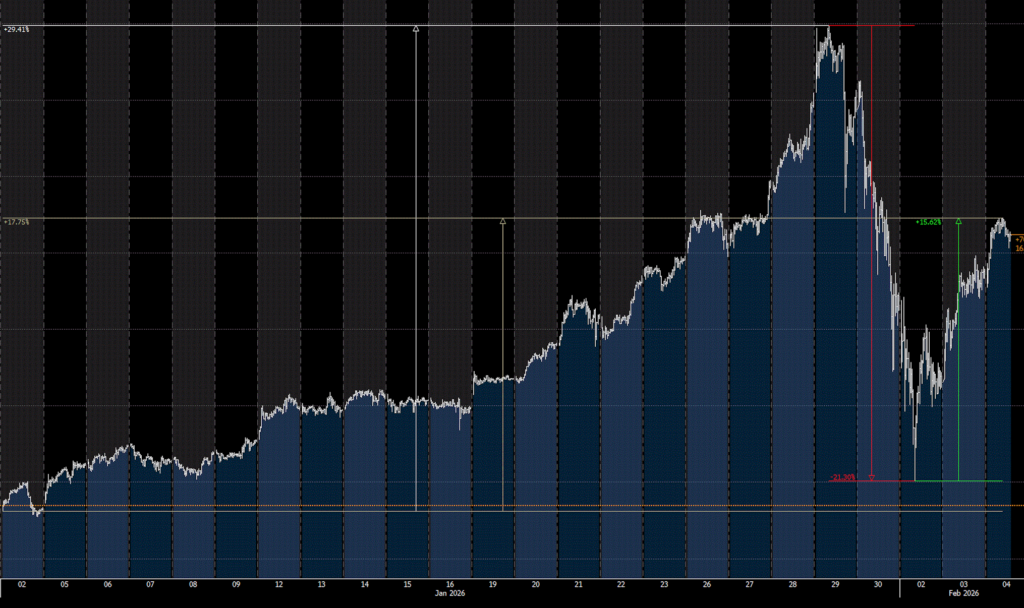

The commodity markets concluded the first month of 2026 with a movement that will be etched in history. Prices of precious metals — notably gold and silver — experienced double‑digit percentage declines over the course of two trading days. The extraordinary nature of this event is underscored by the fact that gold price volatility indicators surged to their highest levels since the pandemic.

This exceptional volatility spilled over from the commodity sector into other asset classes, paradoxically including cryptocurrencies and equity markets. However, by the 3rd and 4th trading days, the situation began to stabilize, as evidenced by signals from the retail market, where the sharp drop in gold prices primarily motivated buying activity among retail investors. This echoed the scenario from the previous week, when social media chatter surrounding the potential forcible occupation of Greenland triggered a shock in equity markets, yet retail investor demand seemingly anticipated the retreat ultimately demonstrated by the U.S. administration in its address at the World Economic Forum in Davos (WEM Research provided live commentary, with the recording available here).

As noted in our previous report, 2026 is poised to be a year characterized by elevated geopolitical risks. External shocks, particularly those driven by geopolitical factors, typically exert short‑term effects on financial markets. This does not preclude their potential to initiate more substantial corrections, which are reasonably anticipated following the attainment of new historical highs. Consequently, 2026 will require investors to be prepared for an increased incidence of volatility.

The episode involving gold (and silver) prices at the turn of January and February serves as a timely reminder of the necessity for an adequately long‑term investment horizon, as well as an appropriate tolerance for market risk. More importantly, it underscores the importance of distinguishing between short‑term crowd‑driven market dynamics and shifts in structural fundamental factors that have been driving the prevailing trend. This holds true even in cases where the trend’s pace may appear excessive, as exemplified by the multi‑percentage‑point daily gains observed particularly in the latter half of January.

As highlighted in our regular “Chart of the Week” feature (see here), the magnitude of gains in precious metals, including gold, appeared overstated from a historical perspective following January. At the year‑end transition, the total capitalization of gold relative to the U.S. M2 money supply reached its highest level since the 1930s (171%).

This also evoked concerns regarding the accelerated pace at which gold and other precious metal prices rose during January 2026. The sharp correction in the final two trading days of January was further fueled by speculation that the announced successor to the Fed chair would not pursue such a loose monetary policy as seemed likely based on the White House’s critical campaign against the current Fed chair, Jerome Powell.

It is therefore prudent to revisit the full spectrum of structural drivers that contributed to last year’s gold rally (and, indirectly, to that of other precious metals).

In recent years, global central banks have intensified their gold purchases. According to the World Gold Council, from 2022 to 2024, they acquired an average of over 1,000 tons annually (more than 800 tons in 2025), compared to an average of more than 400 tons per year from 2010 to 2021.

The ongoing saga of Russia’s aggressive invasion of Ukraine, the onset of U.S. trade wars with major trading partners, airstrikes on Iran’s nuclear program, and tense domestic political situations in Europe’s largest economies last year once again highlighted how rising geopolitical tensions bolster demand for gold. New Year’s events in Venezuela and mass protests against the ruling regime in Iran have reinforced the relevance of this argument early in the year.

In the investment landscape of the previous century, a prevailing rule held that amid heightened economic or geopolitical risks, investors sought refuge in so‑called safe‑haven assets — those resilient to adverse influences. Among the most prominent were government bonds from the largest economies with top investment ratings, particularly US Treasury securities.

Several key policy decisions by the new administration (beyond tariffs, including significant tax reductions) pose serious risks to medium‑term fiscal and debt sustainability overseas. Moreover, rhetoric surrounding the planned conclusion of the central bank’s term raises questions about the previously effective balance between fiscal and monetary policy. In such an environment, gold (and other precious metals) has emerged as the primary remaining “safe haven.”

The aforementioned fiscal policy loosening — faced not only overseas but globally — coupled with recent experiences of abrupt supply shocks in energy and agricultural commodity markets, has stoked fears regarding the future sustainability of inflation. Inflationary pressures are textbook drivers of gold demand, given constraints on its supply.

Similar concerns exist regarding structurally increased budget deficits, which may not be as easy to curb as we have seen in Slovakia over the past three years. At the same time, there are growing concerns that, apart from inflation, there may ultimately be no other option than the so-called monetization of public debt, i.e., the purchase of bonds for central bank balance sheets. This is also linked to the so-called process of de-dollarization—the general weakening of the US dollar not only against other currencies, but also the process of diversifying foreign exchange reserves. In recent years, there has been an inversely proportional relationship between the weakening of the dollar and the appreciation of precious metals.

The proliferation of exchange‑traded funds (ETFs) has enhanced accessibility to gold investments for retail investors. Massive inflows from small investors into these ETFs have been among the most conspicuous factors in the gold price rally.

While this factor may be transient, current constraints on expanding production from existing gold mines represent key determinants of gold price dynamics. Last year’s reduction in dollar interest rates, along with expectations of continued accommodative monetary policy — or even further rate cuts — heightened economic uncertainty, and the so‑called “debasement trade” (shifting capital from fiat currencies to tangible assets, including precious metals) complete the set of primary arguments underpinning the gold rally of recent years.

The majority of these factors are structural rather than cyclical in nature. Many remain relevant this year, though questions persist regarding their intensity and timing. Nonetheless, the excessively rapid strengthening in January over mere days serves as a reminder that investors must anticipate periodic corrections even in precious metals markets. Given the liquidity levels and the breadth of interest that commodity markets have attracted since the onset of the Russian invasion, such corrections could reach magnitudes akin to that of January 30, 2026, when prices moved nearly 8% within 30 minutes. From a twentieth‑century perspective, this represents a historically unprecedented swing for precious metals markets.

Early last week, investment bank Goldman Sachs advised clients to realize gains from prior appreciation while simultaneously raising its year‑end gold price forecast to $5,400. This week, following the sharp correction at the January – February cusp, JP Morgan affirmed its expectation of gold prices rising to $6,300 by year‑end. In recent years, amid broad‑based asset appreciation, passive investing — via purchases of index ETFs and “riding” the upward wave across virtually all markets — has surged in popularity.

The acute turbulence in precious metal prices over the past two weeks thus provides an important reminder that 2026, owing not least to geopolitical tensions, may introduce unusually elevated volatility to markets. Last April’s “Liberation Day” served as a similar warning. In such an environment, the importance of active and professional portfolio management is growing.

The January experience of multi‑percentage‑point daily gains inadvertently evokes the proverbial Wall Street anecdote: when even the shoeshine boy offers investment advice, it is time to exercise caution.

Source: Wealth Effect Management; Chart sourced from the Bloomberg Professional Terminal.

Chief Economist